Skip to content

Skip to content Table of Contents

Every fintech that has crossed the Series A threshold has a version of the same story. The product works. The team is growing. Customers are onboarding. And then somewhere between hiring the 20th employee and preparing for the first enterprise audit, the cracks in the IT foundation start to show. A misconfigured cloud environment. A compliance requirement nobody owned. A security incident that took three days to contain because there was no documented response process. The infrastructure that was good enough to launch is no longer good enough to scale.

This is not a failure of ambition. It is a failure of sequencing. Fintech startup IT support is one of the most consistently underinvested areas in the early growth stage, and it is also one of the areas where the compounding cost of underinvestment shows up fastest. The decisions made about IT infrastructure, security, and compliance in the first two years do not just affect operations. They affect fundraising, enterprise sales cycles, regulatory standing, and the speed at which the business can enter new markets.

This guide breaks down what mature fintech IT management actually looks like, what the core components are, and how to think about building or sourcing that capability as the business scales.

Introduction: Why IT Infrastructure Decides Whether a Fintech Scales or Stalls

Building a fintech product is one challenge. Scaling it under the weight of regulatory obligations, customer data responsibility, real-time transaction demands, and relentless uptime expectations is a completely different problem.

Most fintech startups hit their first serious friction not from product-market fit issues, but from infrastructure gaps. A payment gateway goes down during peak traffic. A compliance audit reveals unencrypted data at rest. A vulnerability sits unpatched for weeks because nobody owned it. These are not edge cases. They are predictable failure points for any fintech growing faster than its IT foundation.

This is precisely where fintech startup IT support shifts from a cost line to a strategic lever. The question is not whether to invest in it, but how to structure it so it grows with the business rather than becoming a bottleneck.

The IT Challenges That Are Specific to Fintech

A SaaS company and a fintech company are not the same kind of business from an IT perspective. The stakes are different.

Fintech operates at the intersection of financial data, personal identity, and transaction velocity. That combination creates four distinct pressure points that generic IT support is rarely equipped to handle:

Regulatory and compliance exposure

Whether a fintech is operating under PCI-DSS for payment data, SOC 2 for enterprise trust, GDPR for European users, or a growing web of regional open banking frameworks, the compliance surface is wide and constantly shifting. Gaps are not just fines. They are license-threatening events.

Security threat specificity

Fintech is not attacked the same way a retail company is. Credential stuffing against authentication APIs, API injection attacks, synthetic identity fraud at the application layer, and insider threat vectors targeting financial transaction data are all disproportionately directed at fintech infrastructure. Generic endpoint protection does not address this threat model.

Uptime as a financial obligation

A two-hour outage for a content platform is embarrassing. For a payment processor or a lending platform, it is a direct financial and reputational event. Fintech SLAs demand infrastructure design, monitoring, and incident response that treats uptime as mission-critical, not just a best practice.

Speed of product iteration versus stability requirements

Fintech engineering teams push fast. New features, new market expansions, new integrations. Each of those creates attack surface and compliance scope. The IT layer needs to keep pace without cutting corners that regulators or security auditors will later find.

This is the gap that fintech managed services are specifically designed to close.

What “Managed IT” Actually Means in a Fintech Context

The term managed services gets used loosely. In fintech, it needs to mean something specific.

Managed IT fintech is not just remote helpdesk support or server monitoring. At the scale-up stage, it encompasses proactive management of cloud environments, security posture, compliance controls, vendor relationships, and IT operations, with teams that understand the regulatory and technical context of financial services.

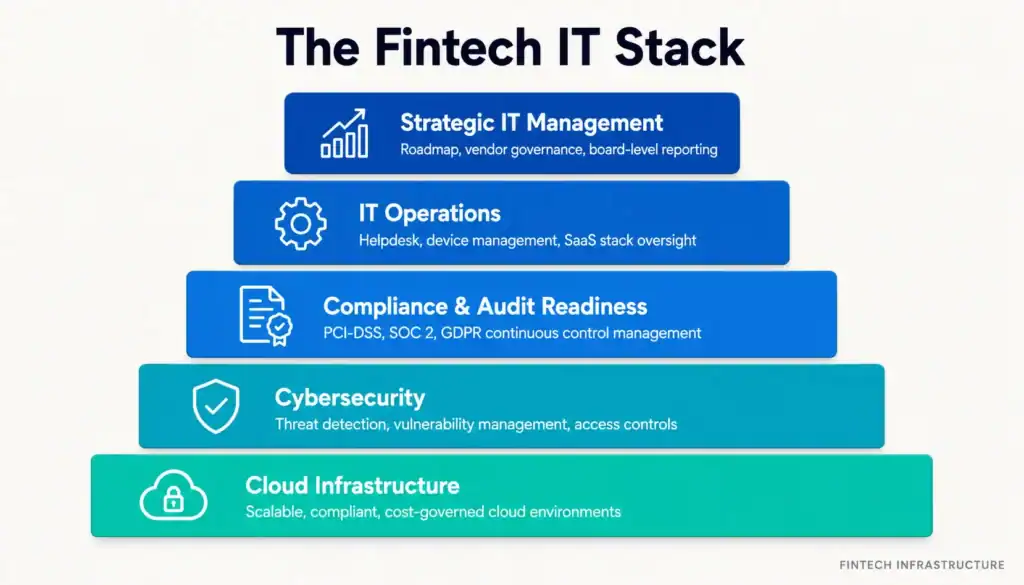

A managed services provider working with a fintech startup should be able to operate across four service pillars without treating them as separate engagements:

- Cloud infrastructure management – provisioning, cost optimization, performance, and disaster recovery

- Cybersecurity services – threat detection, vulnerability management, identity and access controls, incident response

- Compliance services – control frameworks, audit preparation, evidence collection, policy documentation

- IT operations – device management, onboarding/offboarding, SaaS stack management, and escalation support

When these four pillars are fragmented across different vendors, the coordination cost alone becomes a risk. A security event that requires infrastructure changes and compliance documentation should not require three separate vendor calls and a project manager to coordinate them.

Fintech Cloud Infrastructure: The Foundation That Either Enables or Constrains Scale

The architectural decisions made at the $1M ARR stage have a way of becoming constraints at the $10M ARR stage. Fintech cloud infrastructure choices are particularly consequential because they affect not just performance, but regulatory scope, security posture, and auditability.

A few things that separate a well-managed fintech cloud environment from a generic one:

Data residency and sovereignty: Regulations in multiple jurisdictions require specific data to be stored and processed within defined geographic boundaries. Cloud infrastructure that is not deliberately architected with this in mind creates retroactive migration headaches and potential compliance violations.

Segmentation and blast radius control: Financial transaction data, PII, and internal tooling should not share network segments. Proper environment segmentation limits the scope of any breach and makes compliance audits significantly simpler.

Cost architecture: Cloud spend is one of the fastest-growing cost categories for scaling fintechs. Managed fintech cloud infrastructure should include right-sizing, reserved instance planning, and spend anomaly alerting. Unmanaged cloud costs at the Series A stage are a predictable problem. Managed environments tend to run 20 to 30 percent leaner because of proactive governance, which directly affects runway.

Disaster recovery and RTO/RPO alignment: Fintechs often discover their disaster recovery posture during an incident rather than before one. A managed provider defines and tests recovery time and recovery point objectives against the actual business requirements, not just what was technically easiest to configure.

Cybersecurity and Compliance: Where Fintech Cannot Afford to Treat These as Separate Functions

Cybersecurity and compliance are organizationally separated in many larger enterprises. For a fintech startup, that separation is a luxury that creates risk.

Fintech cybersecurity services need to be compliance-aware by design. A penetration test is only useful if the findings map to controls relevant to the compliance framework the business is working toward. An access control audit is only valuable if the evidence it generates is formatted for the auditor.

The compliance landscape for fintechs has become more complex, not less, over the past few years. PCI-DSS v4.0 introduced significant changes around authentication requirements and network security controls. The SEC’s cybersecurity disclosure rules have raised the bar for governance documentation. Emerging open banking regulations in multiple regions are introducing new API security and data sharing requirements.

Fintech compliance services that are delivered reactively, right before an audit, are significantly more expensive and less effective than ongoing compliance management. A mature managed IT provider maintains control evidence continuously, flags drift from baseline configurations automatically, and reduces audit preparation from months to weeks.

Cybersecurity is also not a static investment. Threat actors targeting fintech have become more sophisticated. Social engineering targeting finance and operations teams, supply chain attacks on third-party integrations, and exploitation of misconfigured cloud storage are regular attack vectors. Fintech cybersecurity services must include ongoing threat intelligence, not just periodic scanning.

What to Actually Look for in a Fintech IT Management Partner

Fintech IT outsourcing decisions are often made under time pressure, right after a compliance flag or a security incident. Choosing a partner from that position tends to produce choices based on urgency rather than fit.

The criteria that matter for a fintech looking to scale:

Domain specificity: A general IT managed services provider and a provider with fintech experience operate differently. Ask specifically about PCI-DSS environment management, cloud security posture for financial data workloads, and experience supporting compliance readiness. Vague answers here are informative.

Ownership of outcomes, not just tasks: The right partner proactively flags a misconfigured S3 bucket, not just responds when asked to check. Fintech IT management that is reactive is not managed IT. It is expensive break-fix support.

Documented SLAs for financial workloads: Response times, escalation paths, and escalation ownership should be in writing. The SLA for a production payment environment incident is not the same as a dev environment issue.

Auditability of the IT environment: Everything the provider does should produce evidence. Configuration changes, access reviews, patch status, incident timelines. This is what makes compliance audits fast and clean. If a provider cannot describe how their work is documented for audit purposes, that is a significant gap for fintech.

Integration with engineering workflows: Fintech infrastructure does not sit separate from product. A managed IT partner that cannot work alongside an engineering team using Terraform, CI/CD pipelines, and containerized workloads will create friction rather than reducing it.

The Cost Dimension: What Fintech IT Outsourcing Really Looks Like Against In-House Build

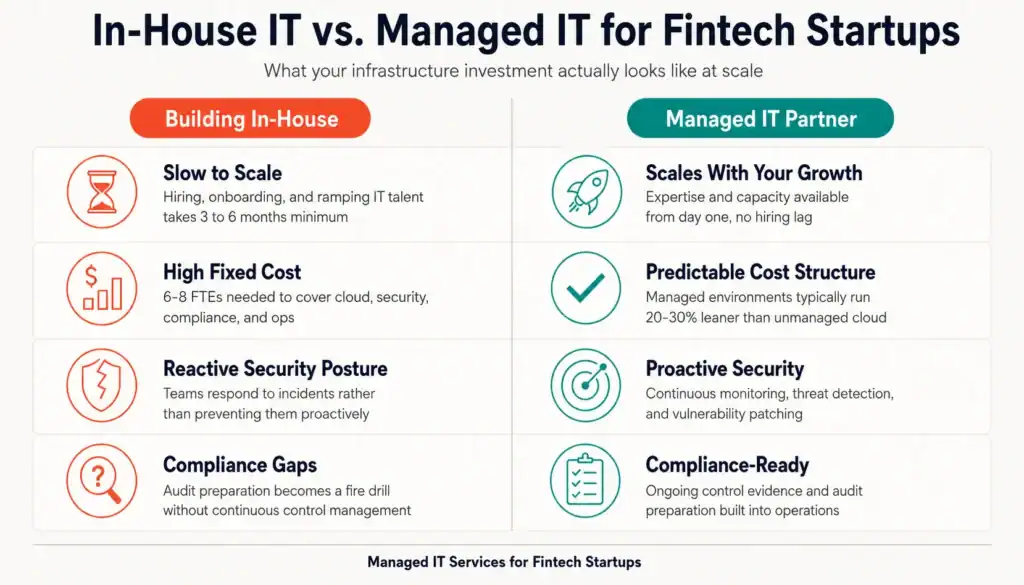

One of the clearest points of clarity for fintech leadership is the build-versus-buy analysis for IT capability. The instinct to build in-house is understandable, but the numbers rarely support it at the startup stage.

A mid-level IT security engineer in a major tech hub commands $120,000 to $160,000 annually before benefits, equity, and management overhead. A compliance manager with fintech experience adds another $100,000 to $130,000. A cloud infrastructure engineer is in the same range. A team capable of covering the four pillars described above would require six to eight full-time hires at the startup stage, with total loaded cost well above $800,000 annually.

Fintech IT outsourcing through a managed services provider typically delivers coverage across all four pillars at a fraction of that cost, with the additional benefit of institutional knowledge, tooling, and process maturity that takes years to build internally. The budget efficiency argument is clear. So is the speed argument. A fintech that needs to demonstrate compliance posture to close an enterprise customer in 90 days cannot hire and ramp a team in that window.

The real question is not whether to outsource, but which capabilities to keep close and which to manage through a partner. Most scaling fintechs benefit from keeping strategic IT decision-making internal while outsourcing execution, operations, and specialist functions like security and compliance management.

Conclusion: Infrastructure Is a Growth Decision, Not Just an Operational One

The fintechs that scale cleanly are not necessarily the ones with the best products. They are the ones whose infrastructure keeps pace with their ambition. That means cloud environments that are cost-efficient and audit-ready, cybersecurity that matches the actual threat model, compliance posture that does not slow down enterprise sales, and IT operations that support the engineering team rather than creating friction for it.

Fintech IT solutions are not a commodity. The provider that manages a fintech’s infrastructure needs to understand the regulatory environment, the security threat model, and the product velocity that characterizes the sector. That combination of domain expertise and technical execution is what separates a genuine managed IT partner from a generic IT vendor.

If you are evaluating how your current IT infrastructure supports your next growth stage, exploring what a purpose-built managed services fintech engagement looks like against your current setup is a useful starting point. We work with fintech startups and scale-ups to build and manage the infrastructure foundation that growth requires. Talk to our team to understand what that looks like for your specific environment.

Ready to see how Zazz can transform your IT operations? Schedule a consultation with our enterprise IT specialists today.